April 24, 2023 by Aaron Winnell

A Medicare Set-Aside (MSA) is a device intended to fund expenses in the future, but it’s a product of the here and now. MSAs are priced based on today’s costs. But inflation assures that tomorrow’s healthcare costs will outstrip today’s healthcare costs. So, it should be no surprise that MSAs are likely to run out of money earlier than projected. That usually means both Medicare and the beneficiary will be stepping in to pay when the money runs out.

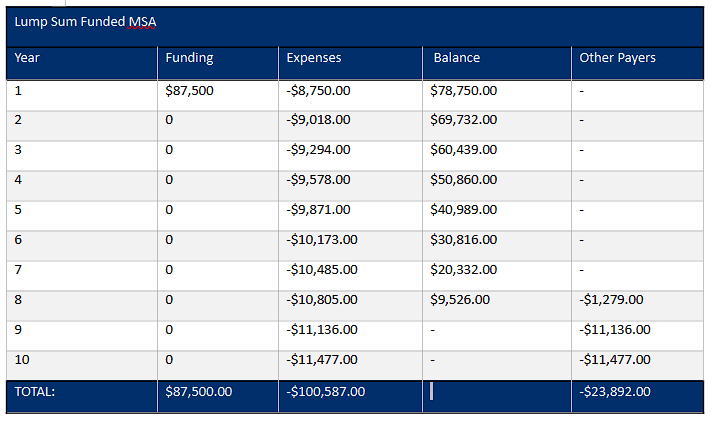

Example 1: Lump Sum Funded MSA

Let’s consider a lump sum funded $87,500 MSA for an individual with a life expectancy of 10 years. That’s an average of $8,750 a year in funding to match expenses. The U.S. healthcare inflation rate in January 2023 was 3.06%. Assuming treatment matches the allocation and inflation remains constant, healthcare costs will be a little over 3% higher the next year, and each year following. The table below shows the impact that inflationary healthcare costs have on a Medicare Set-Aside arrangement that, by its standard projection methodology, assumes flat costs across a fixed period.

As we can see, expenses will exceed the available balance by the eighth year and the MSA fund will permanently exhaust. Another payer, preferably Medicare, will become responsible for their share of the beneficiary’s medical expenses and the beneficiary will begin paying Medicare co-pays.

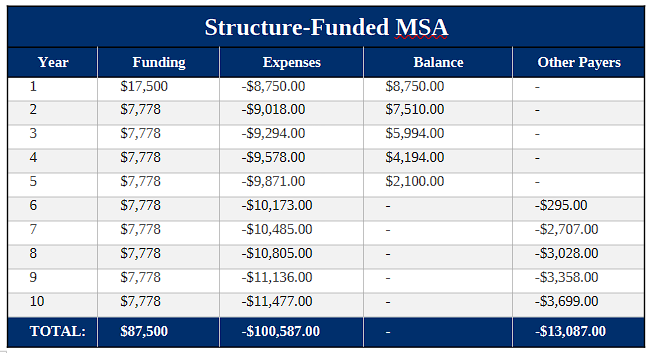

Example 2: Structure-Funded MSA

Let’s take the same MSA from Example 1 and schedule the funding through a structured settlement annuity. The expected average annual expenses and the healthcare inflation rate will be the same.

We observe two differences in Example 2: First, because the MSA fund is not fully funded up front, the toll of inflationary healthcare costs is felt earlier, but the impact is less severe. Instead of permanent exhaustion in year 8, we begin to see temporary exhaustion in year 6. In each year that follows, the structured annual payments are inadequate to cover the ever-higher healthcare costs. But over the life of the MSA, the total deficit is less than if the MSA was lump sum funded.

Perfect is Probably Not Good Enough

These examples demonstrate how aggressive a self-administering beneficiary will have to be to stretch their MSA funds over the course of their life. Even if their medical providers were to stick to the healthcare regimen contemplated by their MSA (uncommon) and the beneficiary only pays for Medicare allowable, injury-related expenses (thankfully, all beneficiaries are formulary experts) at the fee schedules used to price their MSA (beneficiaries know medical coding and billing, right?), healthcare inflation means they will eventually need Medicare coverage for their injury-related healthcare expenses, and that means Medicare co-pays up to 20%. Snarky parentheses aside, a beneficiary might have to dig into their own pockets for thousands of dollars in copays over their lifetime, even if the MSA administration is perfectly compliant.

Professional Administration Can Be a Hedge Against Healthcare Inflation

Many people think that professional administration is mostly a tool to ensure compliance and protect both Medicare’s interests and the beneficiary’s benefits. But a professional administrator can also obtain considerable savings on healthcare expenses over the life of the MSA. This secondary benefit enhances the first for both Medicare and the beneficiary because if the MSA stays solvent, neither the beneficiary nor Medicare will have to pony up for Medicare allowable, injury-related expenses.

As a professional administrator, Medivest applies a number of strategies to contain the rising costs of healthcare faced by beneficiaries. These include, but are not limited to, pharmacy benefit management relationships, supply and equipment vendor relationships, healthcare networks, negotiation, and system tools that look for excessive rates, inaccurate rates, and double billing. Probably one of the most underappreciated aspects of professional administration is the administrator’s ability to negotiate and obtain payment terms through good communication and establishing rapport with healthcare providers.

Professional administration is more affordable today than it has ever been. And in the face of rising healthcare costs, it may be reasonable to argue that most Medicare set-asides can’t afford to do without it. If you would like to begin the process of setting up a MSA for professional administration or have additional questions about how, in most cases, Medivest is able to stretch the lifespan of a MSA please call us at 877.725.2467 or reach out to us here.